On Jan 24, 2023, Hindenburg Research in its Report titled “Adani Group: How the World’s 3rd Richest Man Is Pulling the Largest Con In Corporate History”, highlighted the way the Indian conglomerate remained engaged in a brazen manipulation of stock prices and accounting fraud scheme over the course of decades. Interestingly, The Adani Group’s modus-operandi bears a stark resemblance to a fraudulent scheme woven in Pakistan way-back in 2007-08 by one of Pakistan’s major business players — the Jahangir Siddiqui Group.

In 2008, the Jahangir Siddiqui & Company Limited (JSCL) issued 22,020,000 shares as right to foreign investors at the price of Rs475, inclusive of premium amount of Rs465 per share, having a total value of Rs10.459 billion-equivalent to USD 167 million then. Through manipulation, the price of JSCL share was jacked up to Rs.1326 as of Jan 31, 2008 which subsequently crashed to just Rs.4.0.

Prior to the rights issue, the share price of JSCL was considerably jacked up and daily high turnover was demonstrated to give the impression of liquidity. The share prices of various companies owned by JSCL were also jacked up to show high net-asset value. It may be noted that the capability of the group to generate high turnover is already demonstrated in the Azgard-Nine enquiry report prepared by the Securities and Exchange Commission of Pakistan (SECP) which highlights the fake turnover among various companies and individuals used by the group.

The artificial increase in price of group companies resulted into increase in Net Asset Value of JSCL, and hence high earnings per share of JSCL were reported, misleading E.P.S. trapped investors.

Among the foreign investors trapped in this fraud were various institutions, including a Singapore-based charity institution. The massive losses to the foreign institutions disgruntled them and became a bad publicity for the country, affecting foreign investment.

The Company’s sponsors had not subscribed to the right shares and obtained a waiver from the SECP. The then SECP’s Executive Director Tahir Mahmood — who accepted his role in distributing cash bribes to the fraudsters in the EOBI NAB Reference — was allegedly involved in manipulating the working papers to provide illegal exemptions to the JSCL.

Misrepresentation in JSCL’s Financial Statements

JSCL recorded artificial gain through sale and purchase of shares of subsidiaries and associated companies in 2008 on the pretext of saving capital gain tax in subsequent years, thereby showing artificially inflated EPS, though there was no change in beneficial ownership. Can this be treated as income or was it a violation of accounting principles/standards, misleading EPS trapped innocent investors as well.

Misleading NAV

Similarly Net Asset Value (NAV), as reported in directors’ report for the year ended June 30, 2008, was also misleading as share prices of group companies had been artificially inflated. Foreigners were also misled, who subscribed right shares.

Manipulation of JSCL share price through artificial turnover

The JS Group, in order to manipulate price of JSCL share, initially jacked up price of companies wherein it has substantial stakes such as JS Bank, JS Investment, Bank Islami, the EFU Life, EFU General Insurance, Pak Reinsurance, Azgard-Nine Limited, and JS Global Capital Limited. Various tools were employed to jack up group company prices such as generating artificial turnover, creating a sense of liquidity in those shares. Intra-company investments were made and mutual fund under the management of the JS Investment Company as well as funds available with the NGO, Mahvash Jahangir Siddiqui Foundation were used to pump liquidity in JS Group shares. It then used the high price to issue shares (other than rights) to foreign investors and inflicted huge losses to them.

The artificial increase in price of the group companies resulted in an increase in Net Asset Value of JSCL, and hence high earnings per share of JSCL were reported, misleading E.P.S. trapped investors.

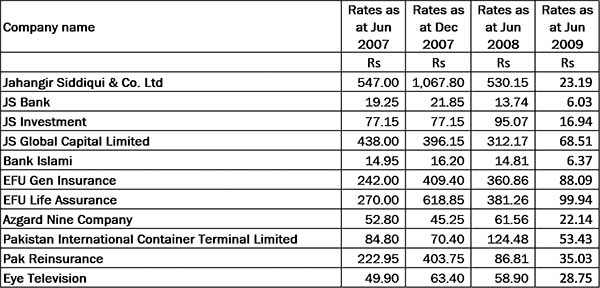

Table-2 depicts the status of share prices of JSCL and companies where it had substantial stakes.

Table 3 illustrates the techniques used by the JS Group to inflate price of JSCL:

However, the increase in value of JSCL shares was artificial. The JSCL share that was jacked up to Rs.1370 per share in the first-quarter of 2008, went down to Rs.21 by the first-quarter of 2009. This affected the market sentiment, afflicting colossal losses to the capital market, investors, public institutions and the national economy. Since there was outflow of foreign investment, the rupee also came under pressure and consequently foreign reserves as well balance of payment were affected.

Colossal losses to Foreign Investors

Foreign Investors incurred a loss of Rs $167 million approximately, which as per current exchange rate amounts to 45 billion rupees. Through this scam reported in 2008, foreign investors were trapped which shook their confidence, as a result of which they started pulling out their investment from Pakistan.

Subsequent event proved manipulation

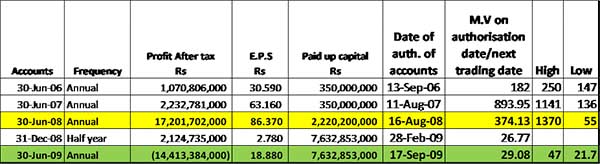

Annual report for the year ended 2009 shows impairment of Rs.16.7 billion proving that the gain recorded in 2008 was artificial, manipulated, misleading, and fraudulent. Further investment in JSIL and JS Global was not fully impaired (which would have further increased the loss due to impairment).

Artificially inflated earnings could not sustain

Table 5 below present how artificially jacked up earnings did not sustain and went down the very next year.

Backing out of ‘Buy Back Offer’

After the right issue, JSCL announced to buy back 7.0 million shares at the rate of Rs.356.32 per share in 2008. But it backed out of the offer on the pretext that it was not approved in the AGM, which is surprising considering that the JS Group was the majority shareholder.

Was the buyback announcement to influence share price and provide exit to someone? Was this announcement intended for manipulation? These remain pertinent and unanswered questions.

The SECP did not take any notice, while the JS Group used this trick to deceive shareholders and sold shares in the market at higher prices through the alleged benami accounts. The trail of their practices of benami accounts is available in the SECP’s report relating to the Azgard-Nine Share price manipulation Investigation report filed in the court.

How was the bubble created?

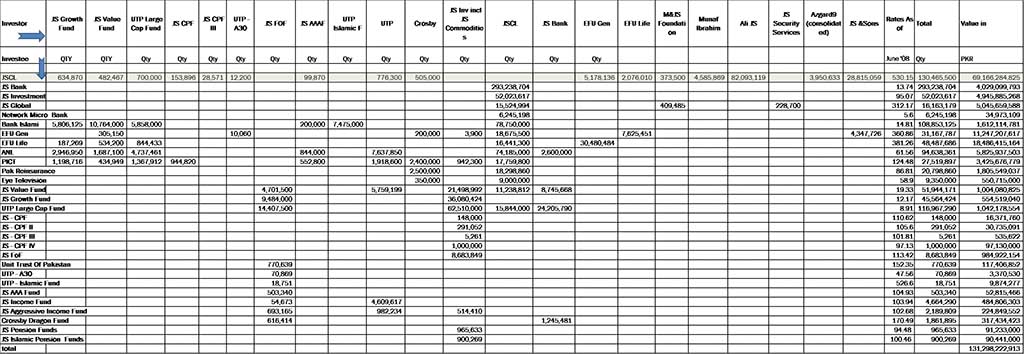

Artificial increase in the value of related companies resulted in an increase in the net-asset value of JSCL through which investors were lured into investing in its shares. The table 6 shows investment made by group companies and associates in each other creating a bubble of billions of rupees, in this case it is precisely Rs 131 billion. The figures have obtained from the published reports of JS managed Mutual funds, Annual Reports of JSCL, JS Bank, JS Global Capital, JS & Sons, JS Securities Services, EFU Gen Insurance, EFU Life Insurance and SECP Reports.

SECP favours the JS Group

While manipulation in JSCL prices was going on, JSCL approached the SECP for issue of rights of JSCL Shares to foreign investors. JSCL CEO Munaf Ibrahim in his letter EW-FH-MI/2008-043 dated April addressed to Tahir Mahmood (then Executive Director/ Head of Department Enforcement) wherein the approval was solicited for the issue of Right shares at premium without subscription of Right by sponsors. The letter also claimed that with the Right issue Breakup value as well as Profitability of the company will enhance. Following projections were given by JSCL which were deceitful as the same were based on investment income from artificially jacked up prices of group companies’ shares:

Within the SECP there was a concern about the premium being charged on the Right Issue and reluctance of the JSCL sponsors to subscribe to the Right Issue. Prior to the right approval request, through manipulation, the price of JSCL share was jacked up to the level of Rs.1326 as of January 31, 2008 which was raising a lot of suspicions. Table 8 depicts the trend of JSCL share price from 2007:

JSCL submitted application to the SECP recommending relaxation of sub-rule (iv) of rule 5 of the Companies (Issue of Capital) Rules, 1996 in order to enable the Company to issue right shares at a premium above the free reserves per share without obtaining undertaking from at least 40 percent of its shareholders, entitled to subscribe for the rights shares and also without arranging underwriting for the remaining right issue. Fundamental question is that how could premium be allowed over and above Net Asset Value (NAV) of an investment company?

During the period when letter was written to SECP (April 21, 2008), until the approval and relaxation form the Capital Issue Rules was granted by the SECP on May 28, 2008, there was a decline in the value of JSCL share by 29 percent (share price of JSCL was Rs.723 on April 21, 2008 whereas on May 28, 2008 it decline to the level of Rs 516). As per sources, JS Group Chairman Jahangir Siddiqui used his influence over SECP to get this right issue approved along with relaxation from the capital issue rules.